What Is Mortgage Refinancing?

Mortgage refinancing enables borrowers to obtain a new mortgage, often under more favorable loan terms. Borrowers may decide to refinance to capitalize on lower rates, switch loan types or programs, shorten or lengthen repayment terms, or access cash from their property's equity. Before making the switch, factor in your home equity, credit score, and refinancing costs to predict whether refinancing will help you save in the long run.

Top Reasons to Refinance

- Lower Interest Rate: If current market rates fall below your original loan rate, refinancing may deliver meaningful savings. For example, a 1% rate reduction on a $250,000 loan could cut your monthly payment by over $150. Or a .50% rate reduction on a $750,000 loan could save over $200/mo.

- Shorten or Extend Payment Term: You may switch from a 30-year to a 15-year loan, or vice versa, to pay off your home faster and reduce interest costs. A shorter-term loan builds equity faster; a longer-term loan lowers monthly payments if cash flow is tight.

- Switch Rate Structure: If you currently have an adjustable-rate mortgage (ARM) and expect rate increases, you can convert to a fixed-rate mortgage for more predictable payments.

- Access Home Equity: If your home has appreciated and you have equity, you might refinance for a higher loan amount and receive the difference in cash. Cash-out refinances let borrowers tap equity for debt consolidation, renovations, education, or investments. Compared to personal loans or credit cards, home equity funds generally carry lower rates.

- Eliminate Private Mortgage Insurance (PMI): If your home value has increased, you’ve paid enough principal down, or the combination of the two has occurred, you’ll often be able to refinance into a loan without PMI.

- Change Ownership: You may need to refinance if you want to add or remove borrowers. This often occurs after major life events such as divorce, marriage or inheritance.

Factors To Consider When Refinancing

The rates must justify the cost – Refinancing incurs closing costs, fees and sometimes longer repayment term risk. You should calculate how long-it takes to break even on those costs. For example, if closing costs equal $3500 and your monthly savings are $150, you would need just under 2 years to recoup.

How long you plan to stay in the home – If you expect to sell or move soon, a refinance might not pay off. The longer you remain in place, the more you benefit from a lower rate or improved terms. You may also want to consider whether you would rent out your place if you moved and kept the loan.

Your credit profile and loan conditions – If your credit score has improved since you first borrowed, or if you now qualify for a better loan type (e.g., no private mortgage insurance), you may benefit.

When To Refinance

- Falling Interest Rates: The best time to refinance is when market rates fall below your current rate by at least 0.5%. Refinancing jumbo loans can make sense at only .25%, depending on the loan amount.

- Improved Credit Profile: If your credit score has improved since your original loan, you may qualify for better pricing and terms.

- Home Value Appreciation: Higher equity may allow for improved loan terms or a cash-out refinance for major expenses.

- Upcoming Financial Goals: If you need cash to fund renovations, college, medical events, or investments using home equity.

When To NOT Refinance

- Minimal rate improvement: If interest rates are not low enough to offset closing costs, a refinance may not provide net savings.

- Longer loan term: If you extend your repayment period to lower monthly payments, total interest costs may rise significantly.

- Short timeline in the home: If you plan to sell soon, you may not remain long enough to justify refinancing costs.

- Weaker equity position: If you extract cash and accept a higher rate, you may increase monthly payments and reduce equity.

Costs and Break-Even Analysis

Refinance involves closing costs, depending on a variety of factors including whether you decided to pay points. Savvy borrowers calculate their break-even point (by dividing closing costs by monthly savings) to assess whether refinancing aligns with long-term goals. If planning to sell soon, refinancing often does not make sense.

If closing costs are a concern, ask your mortgage advisor if you qualify to have your costs added to your loan amount. A “no cost refi” is usually available at a slightly higher rate to cover your closing costs with a lender credit. Both scenarios allow you to avoid out of pocket expenses when refinancing.

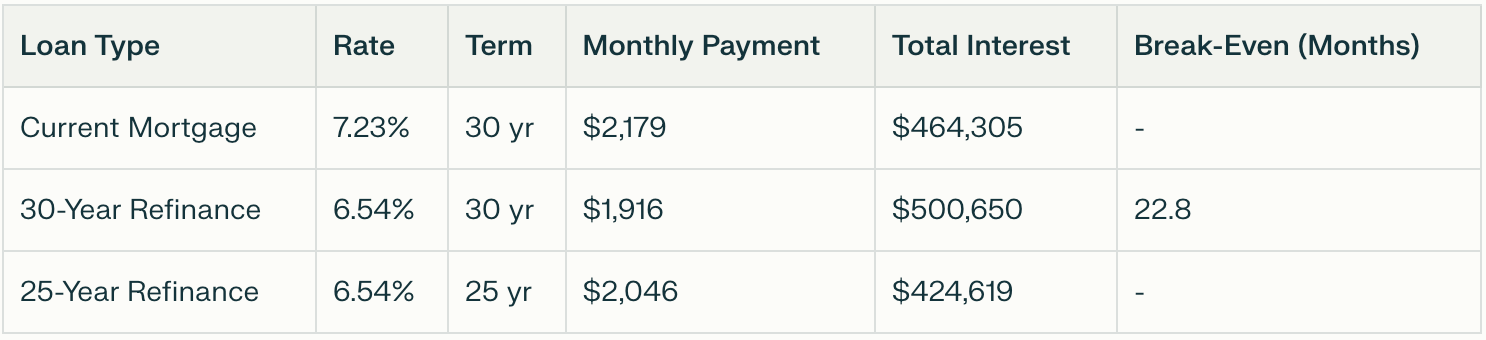

Example Table: Refinance Savings

Pros and Cons of Refinancing

Pros:

- Lower monthly payments

- Potential for shorter loan term and less interest paid

- Manage or eliminate high-interest debt via cash-out refi

- Ability to remove PMI

Cons:

- Potential out of pocket costs

- Temporary dip in credit score (do we want a section where we explain the why or leave as is and deal with that later in an article about credit?)

- May increase total interest if the new term extends the payoff

- Using home equity for discretionary spending can hinder your long term financial goals

Qualifications and Process

Lenders evaluate credit score, home equity (often 20% minimum to avoid mortgage insurance), debt-to-income ratio, and financial stability. FHA, VA, and USDA loans have unique requirements for refinancing frequency and equity. Multiply Mortgage simplifies pre-qualification and tailors solutions to borrower goals.

Should You Refinance?

Refinancing is appropriate when long-term financial benefits, or short term needs, outweigh the costs. Success depends on timing, qualifying, and aligning new loan terms with today’s goals. Multiply Mortgage offers expertise tailored to your unique financial situation, and easy-to-use calculators so borrowers can make informed choices.

For more information or to start your refinance, get in touch with a Multiply Mortgage Mortgage Advisor today.